The Impact of Geospatial Analytics on the Dynamics of Financial Services & Retail Banking

In 2020, the world changed. Any digital transformation that banks and other financial institutions were undertaking accelerated as businesses and customers alike navigated the most efficient way to manage their money during the coronavirus. Retail banking has become more mobile and branches have had to allocate their resources judiciously. Cash is king again but so is e-commerce. Given these changing dynamics, how does the banking industry use geospatial analytics to capitalize on consumer behavior that has adjusted to a new normal?

It all starts with data. In addition to the customer’s basic personal information, financial institutions (FI) are collecting vast amounts of transactional data, such as credit card purchases, almost all of it tagged with a location. These transactions occur at retail establishments, through e-commerce, or a simple deposit from the bank’s mobile app. Every transaction happens somewhere. These pieces of data form the essential backbone of customer analytics. They are especially important as the composition of customers trend towards a younger demographic, with increasing disposable income, that have a greater need for banking services as they mature.

If it all starts with data, what tasks should you tackle first? Sometimes, the most basic information can be the most challenging, for example, a customer’s address. How often do you find, misspelled names and addresses in your marketing database? Do you find missing postal codes or misfielded data, such as a house number where a ZIP code should be? Ensuring that your corporate client address data is of the highest quality, with as few errors as possible will improve the success rate of your campaigns.

What would be possible, if your marketing, real estate and operations teams, could get a more complete view of each branch? What would happen if you could capture data that would permit you to see transaction type, amount and frequency of visits to each branch and segmented by client? Once you have collected all this data, how, then, can banks monetize it? And what are the challenges and pitfalls faced by financial institutions just now leveraging the power of location technology? Let’s look at some of the potential opportunities that allow banks to become more location intelligent.

Geospatial Data for Financial Services Market Analysis

Millennials are mobile and their banking habits reflect a propensity to use mobile banking applications rather than visit a physical branch (refer to figure 1). Baby Boomers still like to visit branches and talk to “real people” to do their banking. As such, marketing to these different types of clients demands an understanding of when, how and where these customers visit each branch in the network. So, it is important to understand the shifts in demand by audience segment in order to deliver services that target specific clients.

Activity Based Marketing & Know Your Customer

There are several requirements to successfully implement activity-based marketing. Marketing programs require extensive use of both current demographic data but also more dynamic, mobile audience movements, such as footfall traffic and dwell time. With this data, it is possible to determine the frequency of visits, the ability to serve pedestrian and vehicle traffic and to consider whether each branch is aligned to serve specific audiences. This information is easily modeled with geospatial analytics and allows for the successful alignment of services.

But how would you target a very specific target audience? Let’s say you wanted to focus on certain high-net worth customers. These higher-income, career-focused-individuals or families with greater disposable income, living in areas where the property values may significantly deviate from the norm, have a greater need for investment services and mortgage financing. Knowing this will allow the branch to staff accordingly and target these individuals with marketing campaigns that attract them to the branch for more information.

Optimize Branches According to their Location and Performance

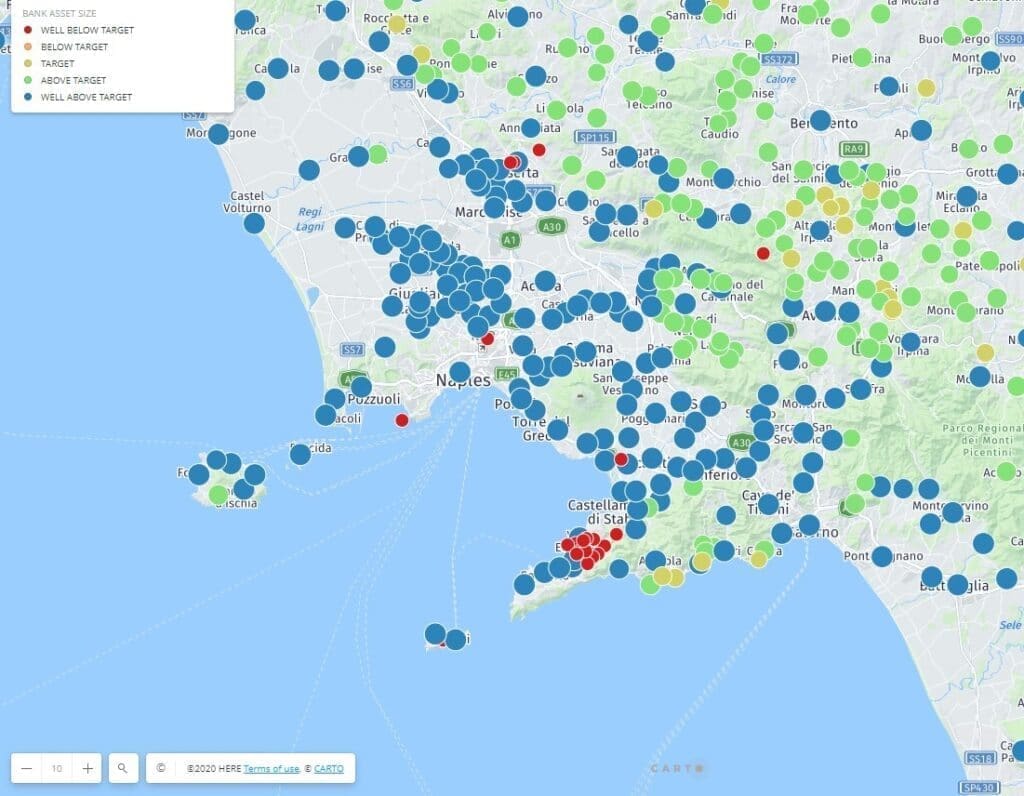

But what would happen if you were able to perform this analysis on each branch? The result is a clear picture of branch performance, the ability to compare the success of each branch and an understanding of why some branches perform better than others (refer to figure 2). Armed with this information, geospatial analytics provides the ability to identify model branches or analogs that show how other branches should perform. But there is more. Depending on the demographic composition of each branch trade area, models will differ. The goal is to align success factors and optimize the network accordingly.

(This figure uses fictitious data to illustrate the ability of geospatial analytics to easily compare branch performance.)

Branch optimization must account for several factors, both related and unrelated to location. These attractiveness factors change over time and must be updated depending on demographic composition, changes to the highest and best use of each property, competition, mergers and acquisitions, and corporate goals. It may be determined that to serve 80% of the company’s clientele effectively, each branch must be located no further than a 7-minute drive-time window. This requires accurate address information for each customer and a comprehensive digital street network as a baseline of geographic information. Location-allocation models are often employed to analyze all factors that contribute to efficient network planning.

Consider for example that the corporation sets new metrics for performance. In order to accomplish this, a new product mix is introduced with the objective of increasing the size of the trade area to capture a greater share of wallet. As a consequence, some branches could be closed, others relocated. However, before making any decisions, you need to think about the impact this will have on the trade area.

- Will clients be left underserved?

- Will accounts be lost to attrition?

- Will the branch network violate regulatory compliance guidelines?

- Will some branches require additional staffing to support new products and the expansion of the trade area?

All these situations must be considered, which means that regular branch network assessment is required to maximize performance.

In the event of a merger, how are business operations impacted at the customer level, if those individuals are account holders at both institutions? Here, entity resolution, a data quality process, resolves duplicate account information. As such, geospatial entity resolution uses a highly accurate address table and geocoding solution that validates, parses, normalizes and standardizes addresses. The process then merges this information into a geographic master data management system for a single customer view. Once configured, this solution becomes a highly effective method for detecting financial crimes.

Map Visualization of Asset & Cash Management

Today, banks are also required to maintain an extensive array of physical assets including ATMs, kiosks, and deposit drop boxes, located adjacent to branches as well as in remote locations. Managing these assets requires servicing and upgrading, as well as understanding the distribution and usage of cash daily. Map visualization of these dynamic conditions makes it easy to identify the serviceability and customer usage.

Sometimes, however, daily snapshots of information provide only part of the analysis. Predictive analytics, using historical transaction data, as well as information such as vehicle traffic volume, changes to income distribution or audience composition and socio-economic conditions can help determine future demand.

As with branch site selection, remote assets have a trade area as well. Certain convenience factors enter the model including but not limited to drive-time, physical barriers such as divided highways, or the side of the street that provides the better ingress or egress.

Risk Management and Fraud – Using Address Management, Address Quality & Precise Geocoding

Where do fraud and location meet? Fraudulent activity in financial services can appear in credit card transactions, mortgage lending practices and cyberthreats. Each of these activities have a location component:

- The delivery address for the online credit card purchases mismatch the billing address.

- The transactions occur far outside the typical geographic region of the credit card holder or in succession at locations far from each other.

- Multiple transactions at a single location may indicate that an employee is skimming.

Supported by geospatial analytics, banks and their customers can be alerted of potential threats.

Imagine the billions of credit card transactions occurring globally, and you quickly realize the nature of a “big data” problem. Solutions that quickly recognize the location, spending patterns, and amounts can be identified through geospatial proximity analysis. These analyses must have a foundation of using accurate geocoding technology that can quickly determine the location, business establishment name, and credit card holder’s address in order to spot fraud. With today’s geospatial solutions, the task is much easier to tackle.

Loan compliance is also a key area where geospatial technology can support lenders. Legislation guides lenders to service loans in all socio-economic classes. Understanding whether the loans being made comply with these regulations can be done through geographic and demographic analysis. Map data will demonstrate the extent and amount of loans geographically.

In addition, mortgage lenders need to be aware of the risks that will impact a property’s propensity to be damaged by fires, floods, earthquakes, wind and other perils. These risks can be modeled based on historical location data that can be enriched by the intensity and extents of each peril. As a result, mortgage lenders can assess whether the property can be appropriately underwritten. Likewise, property and casualty insurance companies will look at the same risk factors to determine policy pricing to assure that the property assets can be covered as a result of a catastrophic event.

Leverage Location Intelligence for Strategic Decisions in Banking and Financial Services

Banks and financial institutions have an enormous opportunity to leverage location-based information to support marketing, compliance, strategic planning and operational tasks. Understanding how to best implement geospatial technology is what we do at Korem. We have helped many financial institutions take the first step toward digital transformation. Contact us today!