Improving the Customer Experience in Banking With Geospatial Technology and Data

There has been talk of a digital transformation and the evolution of consumers’ expectations in the financial services industry for several years now. This phenomenon has accelerated even more so since the COVID-19 pandemic, which has driven banks to rethink their customer services, both online and in person. Now that the use of technology is well established in the market, banks that are slow to remodel the customer experience (CX) find themselves somewhat lagging behind others in modernity and innovation. This delay may directly influence the loyalty and retention level of their clientele, reputation, market share, and their ability to stand apart from the competition.

Currently, several banks wish to invest time and money in obtaining hyper-personalized information for their clientele in order to improve both the customer and user experience. This does not only involve providing them with personalized products but also understanding their overall “financial health.”

Request your geospatial health check today »

New banking customer experience trends

More and more financial institutions want to change their approach and offer a more harmonious customer experience to win back their customers’ trust after the 2008 financial crisis. Currently, 67% of customers around the world frequently access their bank accounts through digital channels, such as mobile banking apps and online banking platforms, and 69% of them would like their whole financial life cycle to be on digital channels.

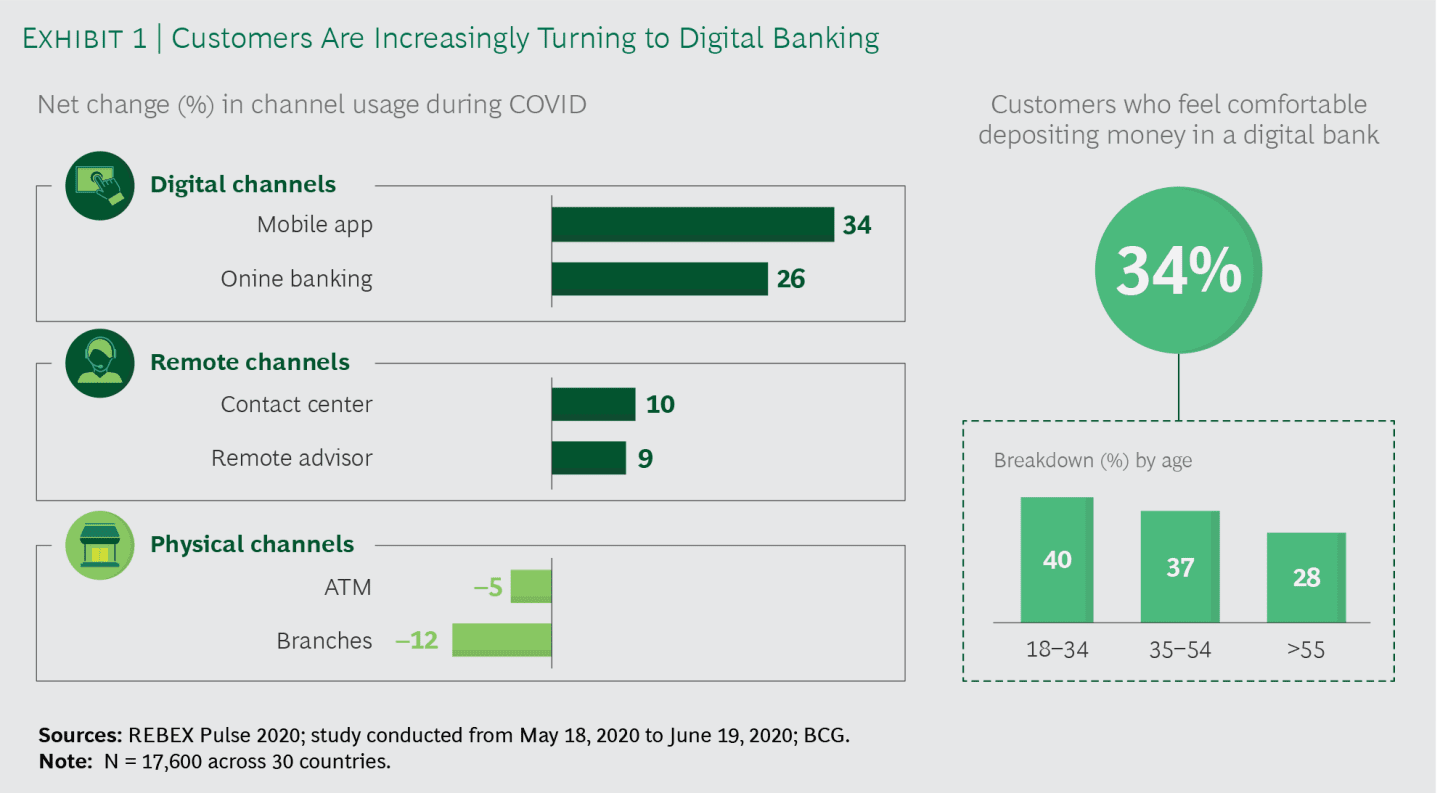

As we can see in the graphs below, customers are becoming more and more used to their financial institution being an app rather than a building. As such, 34% of customers feel at ease depositing money in a “digital bank.” Moreover, during the first six months of the COVID-19 pandemic, the use of mobile banking increased by 34% whilst banking services in branches decreased by 12%.

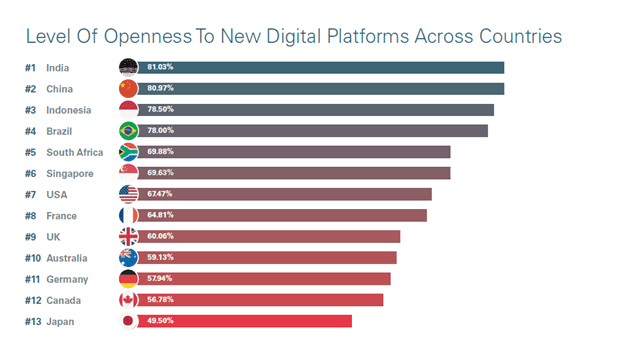

In order to satisfy and retain their clientele, banks must integrate their banking activities into multiple intuitive channels enabling customers to receive a personalized service at all times. However, as the graph below illustrates, the level of openness of banks regarding new digital platforms varies considerably from one country to another. Although the majority of organizations place customer experience as a strategic priority, only 30% of them invest money in understanding and improving it.

It is an important consideration given that, when the requirements and needs of a customer are not met, they may turn to another establishment and encourage their peers to do the same. Several banking customer experience trends may, therefore, appear and be rolled out over the next year to meet new public needs. Here are some of them:

Automated integration

Firstly, we can think about automated integration, which provides the option for customers to follow welcome procedures electronically rather than on paper. Banks then allow them to easily provide all the information necessary for the creation of a new account from the comfort of their home.

When signing up, users can benefit from address management and geocoding functions, which consist of attributing geographic coordinates to a postal address. This enables the automatic entry of addresses for a quicker and more precise transfer of data, along with a reduction in the risk of errors. Financial institutions can then use an automation function so that customers can open their accounts faster when they use the self-service, which has a positive impact on customer satisfaction.

Personalized offers

In addition to helping banks plan their social media marketing campaigns and making more enlightened decisions about their branches, hyperlocalization and datasets, which include among others, demographic data and real-time traffic data, enable banks to better understand their customers and anticipate their needs at each stage of the financial life cycle. They also make it possible to determine which credit limits should be increased, to establish whether a loan to an existing customer should be approved or not, to reduce frictions through different banking processes, and to personalize offers and products. For example, knowing that a customer has visited five car dealerships over the course of the past week, a bank could contact them to make them an offer on a car loan rate.

A McKinsey study has, moreover, proven that customers who receive personalized banking offers in an omnichannel manner are three times more likely to accept them than those who receive them over a single channel.

Details on transactions

Within the framework of their strategy and desire for transparency, banks want to provide their customers with as many details as possible about their transactions. These customers often go into branches not to open a new account or to request a loan, but because they need answers to specific questions that they are unable to obtain online.

A frequent problem is that customers don’t always recognize the transactions on their accounts. This is due to the fact that a transaction through a debit or credit card often appears in the name or telephone number of the merchant category code. Geospatial technology enables customers to go back to the transaction and to obtain the name and address of the company of where they were when they made the purchase, thus providing the customer with peace of mind.

Modeling of banking activity and risks

Large banks all work on data integration and modeling of banking activity and risks to offer a better customer experience and more transparent information. Only a few years ago, this was a different exercise for each branch. Today, they strive to consider internal and external data in a holistic manner and model them in each company. Analysis of these data helps maintain the trust of the clientele and keep the pace of competitors offering exclusively online services.

In the digital era, it is in the interests of financial institutions to improve their modeling exercises with high-quality geospatial data. These data can, in both space and time, describe the movement of people and property, as well as natural events such as hurricanes and viral pandemics, for example.

Why do business with third-party data experts such as Korem?

In order to increase customer retention rate and start a digital transformation in line with their strategy, retail banks are increasingly turning toward precise data. The financial services industry can collect enormous quantities of internal data through banking digital services. However, to maximize their results, financial institutions may find it advantageous to combine them with external data provided by strategic partners, such as third-party data experts. These experts will, therefore, be able to enrich their data, facilitate their integration and make them more freely accessible to minimize risks and ensure proper use.

Korem is perfectly positioned to facilitate your digitization and omnichannel decision-making. We will also help you to obtain, manage and use your data so that you can provide your clientele with a flawless customer-centric experience.