How Geocoding and Location Data Are Transforming Insurance Underwriting and Pricing

March 11, 2025

In today’s world, the insurance industry faces challenges that include rising claims, changing consumer habits, rapidly evolving technology, and increasing regulation. The reputation of these companies is based on their ability to calculate risk as accurately as possible so that the pricing of insurance premiums will yield a balanced book of business. The objective is to remain competitive and reduce churn.

As a result, insurers are increasingly relying on geospatial technology and, more specifically, on hyper-precise location data and geocoding software to improve the policy underwriting process.

To more effectively harness advanced risk modeling and gain a competitive advantage through more accurate policy underwriting, be sure to join our webinar on the utility of geospatial technology in insurance.

Benefits of Geocoding and Location Intelligence for Insurance Companies

1. Take Advantage of Quality Data

Some insurance companies are proud to offer policies at a lower cost than others through automatic underwriting; however, this underpricing, caused by negligence towards accuracy, is not to their advantage. It causes them to underestimate the risk to which they are exposed, which could lead to significant losses and a damaged reputation. Both can be avoided with quality data.

Therefore, to improve underwriting processes, the data used by insurers must not only be operationalized to improve the client experience but lead to lower risk. In general, the best method for assessing risk is not to divide streets into segments and rate all the houses in each segment the same, but to use the latitude and longitude measured at the center of the parcel where each house is located.

In order to do this, it is necessary to rely on several sets of hyper-precise location-based data. In principle, property risk models will lead to incorrect assumptions if real-time location data and ancillary attributions are not included. Even small geographic errors can have a significant financial impact if, for example, addresses are not correctly validated or flood, wildfire, and earthquake zones are not updated.

What types of geospatial data are most useful for insurance or commercial underwriting? For any given location of a personal residence or commercial property, the proximity to key perils must be incorporated into risk models. The location of fire hydrants and fire stations, hazardous material storage sites, or chemical plants can affect policy pricing. In addition, the location of recent claims or crime rates in the area has impacts as well. Geospatial data also includes weather or climate data, earthquake fault zones, or areas susceptible to wildfires. Accurate location data, therefore, allows insurance companies to pre-score the risks of certain geographic areas to mitigate losses thereby increasing their profits and improving the overall health of their book of business.

Further, to correctly estimate policy costs, some companies, such as Belair Direct, use data to create advanced algorithms based on artificial intelligence (AI) and machine learning (ML). AI is useful for helping insurers make sense of big data, especially for underwriting and fraud detection, while ML is used to predict premiums and policy losses. Others, like SSQ Insurance, use a multivariate statistical model instead. Insurers are also collecting telematics data, through mobile devices and apps to determine driving behavior.

Canadian casualty and property insurance company, Desjardins, has leveraged geospatial technology extensively. Using cloud computing, artificial intelligence, access to external data, and advanced P&C insurance analytics, Desjardins was able to model all Canadian waterways and geolocate properties to better model the risk associated with rising water levels. The company is now proactively alerting policyholders to protect themselves against flooding. These tools have also allowed Desjardins to develop the Radar feature, which is available for free in its mobile application, to warn its policyholders of serious weather risks within 500 meters of their property.

2. Linking the Systems

Insurance companies often use an out-of-the-box application to locate homes or vehicles to assess risk and properly apply policy rates. However, Perr&Knight has shown in two studies that there is a significant impact on return on investments (ROI) when companies replace their current application with a geocoding application that delivers hyper-accurate location data in insurance.

Perr&Knight’s results have shown that accurate geocoding could result in 5.7% of homeowners incurring a change in rating territory. While this number may not seem high at first glance, it does correspond to a significant change in the insurance premium for this group of homeowners. Their premium could either increase by 86.7% or decrease by 46.4%, which directly affects the profit of insurance companies and the risk they face if they do not rate their policyholders appropriately.

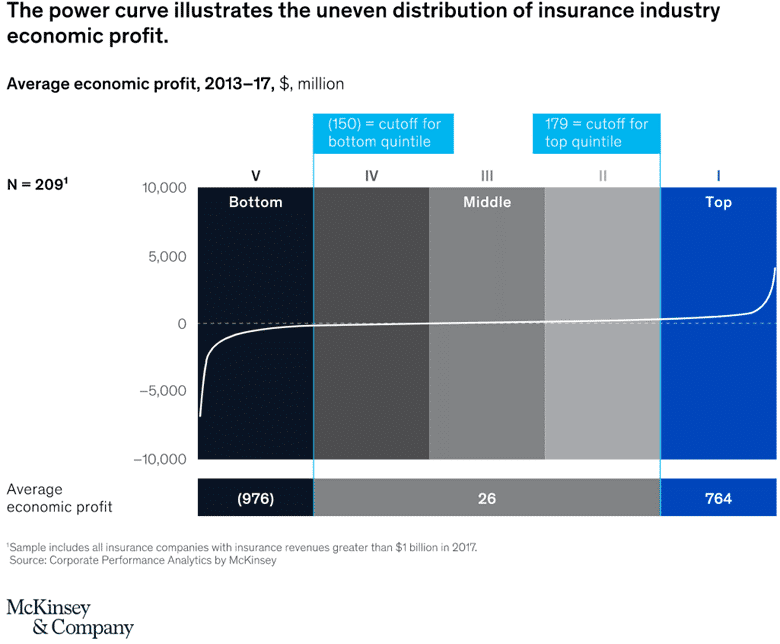

Moreover, according to an analysis of insurers’ economic profit conducted by McKinsey, it was found that insurers’ profit is unevenly distributed from one company to another. As you can see on the diagram below, 60% generated an average of $26 million annually while only 20% managed to make a profit of $764 million per year between 2013 and 2017. The bottom 20% lost an average of $976M annually per company. These loss ratios could obviously have been avoided with a better risk assessment.

Source: McKinsey & Company

3. Increase Productivity

Leveraging geospatial technology has become essential for the insurance industry to increase its analytical capabilities tenfold and manage risk in exceptional ways. Examples of geospatial capabilities include raster modeling for high-risk areas, integration points with P&C insurers platforms, specialized datasets that can be integrated with geoenriched address data, cloud-native data processing, and more.

“Technology is a lever to make processes more efficient, drive productivity gains and create value for customers.”

– Mr. Dubois, President and Chief Operating Officer of Desjardins Insurance Group.

The most prolific insurance companies are using advanced data and analytics to rethink risk assessment, improve the customer experience, and enhance efficiency and underwriting decisions throughout the pricing policy process. They have also deployed sophisticated technologies over the years that allow them to develop effective models and constantly refine them. As an example, Korem helped an insurance leader who wanted to integrate geocoding and address validation functions into its Microsoft Azure software.

Korem proposed a solution combining ready-to-use software and data through the Spectrum platform from Precisely, a supplier of geospatial technology. Spectrum was specifically chosen for this client because it is a high-performance, enterprise-grade, geospatial platform offering a modular and open architecture. This enabled the insurer to facilitate address validation and geocoding, risk management, customer qualification, and insurance underwriting.

The Evolution of Geocoding in Insurance

The insurance industry has always relied on geocoding, as a crucial tool in data-driven underwriting. Traditionally, insurers relied on postal addresses and generalized territorial risk models, which often led to discrepancies in pricing and exposure assessment.

However, modern geospatial technology has enabled companies to move from broad, region-based risk assessments to hyper-localized, property-specific evaluations.

Advanced geocoding for insurance now incorporates:

- 3D mapping technologies to analyze terrain elevation and predict flood risks with greater accuracy.

- Historical climate data to assess how weather patterns impact policyholders over time.

- Real-time satellite, aerial imagery and building footprints to validate property characteristics and detect changes that might affect coverage.

Geocoding and Fraud Prevention in Insurance

Insurance fraud costs companies billions of dollars annually, impacting not only their profitability but also policyholder premiums. Geocoding and insurance location data play a crucial role in mitigating fraudulent claims through:

- Verification of claim locations: By cross-referencing geospatial data with reported claims, insurers can detect discrepancies in property damage reports, especially for weather-related claims.

- Pattern recognition for fraudulent clusters: If multiple high-risk claims originate from the same area within a short period, insurers can flag the zone for further investigation.

- Integration with telematics and IoT devices: Geocoding enhances fraud detection in auto insurance by validating the exact location of an accident against GPS data collected from vehicles.

With this, insurers can prevent fraudulent claims before they are paid out, reducing unnecessary losses and maintaining the integrity of their underwriting processes.

Personalized Insurance Pricing with Geospatial Data

Consumers today expect tailored insurance policies that reflect their specific risks rather than generalized premium structures. By integrating insurance location data, insurers can offer:

- Usage-based insurance (UBI): Automobile insurers can use telematics data combined with geocoding to price policies based on where and how a vehicle is driven.

- Hyper-localized home insurance rates: Instead of basing premiums on ZIP codes or broad geographic territories, geocoding for insurance underwriting allows companies to assess risks on a property-by-property basis.

- Customized commercial insurance: Businesses located near hazardous areas, such as chemical plants or flood zones, can receive policies that align with their precise risk exposure.

This data-driven approach not only optimizes insurance underwriting but also ensures fair and better pricing, making insurance more transparent and adaptable to each client’s unique situation.

Future Trends: AI-Powered Geospatial Analytics

The future of insurance underwriting lies in the convergence of geospatial analytics and artificial intelligence (AI). As geocoding becomes more sophisticated, AI-driven models will further refine risk prediction by:

- Continuously updating geospatial datasets with real-time sensor and satellite data.

- Enhancing climate change modeling to anticipate risks linked to extreme weather events.

- Automating insurance underwriting decisions, reducing human error, and improving operational efficiency.

Companies investing in these geospatial advancements will gain a significant competitive advantage, positioning themselves as industry leaders in risk assessment and customer-centric policy pricing.

Take Advantage of Geospatial Technology

Our team of experts works for you, providing objective, vendor-neutral recommendations. We can maximize your investments through our insurance geospatial health assessment offer, which will help us diagnose your geospatial ecosystem to find effective strategies that are consistent with your needs and goals.

At Korem, we specialize in delivering cutting-edge geospatial solutions tailored to the unique needs of insurance companies. From precise insurance geocoding to advanced location intelligence, our expertise helps insurers enhance risk assessment, streamline underwriting processes, and optimize policy pricing. Whether you need to integrate real-time geospatial data, improve fraud detection, or develop AI-driven risk models, Korem provides end-to-end support to ensure your business stays ahead of the competition.

Get in touch with our team today to learn how Korem’s geospatial expertise can transform your insurance operations. Contact us now and reach out to our specialists for a personalized consultation.